Alright, it’s been too long since I had a huge post (maybe 20 hours) so I thought I’d lay one out again. I’d like to talk about Health Care, and why I’m voting for Obama because of it.

Let me start by surprising everyone who hasn’t talked to me with the following:

I hate Obamacare - I think it violates our rights by forcing us to buy a product from private companies, and probably should be repealed.

“But why are you voting for Obama then Rob? Surely Romney’s repeated calls to end Obamacare appeal to you!” - GOP Supporter

Lets start by looking at our health care system before the Affordable Care Act went into effect.

First - Every person could go to an ER, and that ER would be forced to give them basic life saving care, even if they didn’t have insurance. People still died of cancer and all sorts of nastiness, but hospitals were generally not allowed to turn people away.

Second - Not everyone had health insurance. Some people had preexisting conditions and were denied coverage. Some were unemployed and couldn’t afford it. Some were students older than 24. Some had jobs that didn’t provide it. However, those people still sometimes went to the hospital.

Third - Sometimes health insurance wouldn’t cover a procedure that a doctor recommended. Health insurance companies dictate medicine, not medical doctors.

Anyone with a job most likely has seen their health care costs rising slowly since they’ve ever worked ever. A little raise in their premiums there, an increased deductible there. A new service not covered.

Why you ask? Was this profiteering by insurance companies? Sure, maybe. Profiteering by doctors and hospitals? Maybe. Largely though, the problem was that you received treatment first and were billed second. If your insurance wouldn’t pay and you were stuck with the bill? You could simply declare bankruptcy or just not pay. Of course the hospital still incurred the cost of your surgery. You used medical supplies, Doctor’s time. Anesthesia and band aids. Electricity. All that stuff still had to get paid for.

Lets say you make minimum wage working at Walmart, 30 hours a week. You may have a child. You make too much to be on medicaid, but still can’t afford insurance. Then, you get a large kidney stone, require surgery, and get stuck with a $40,000 bill for surgery. Or you get shot in the face watching batman and incur a 2 million dollar hospital bill. What if you are unable to pay?

The hospitals - some public and some private - do the only thing they can do, which is passing those costs onto the paying customers. And the only ‘paying’ customers were people with insurance. Thus, the bill for any given procedure is largely automatically inflated, because it’s costs if paid must go towards costs of procedures that aren’t paid. That’s one of the reasons Americans spend almost 3x more on healthcare than countries that don’t have our 'system’.

The poorest Americans, the oldest Americans, were covered under Medicare and Medicaid. But there’s a group of people - lower middle class, upper lower class - that may slip through the cracks.

**Ok, so what did Obama care do for us?**

First, it made more people pay into the health care industry. The more people who are paying into the system, the more the health insurance industry can spread those costs across everyone. That means less people who are going to the hospital without health insurance.

Second, it capped the profits of the health insurance industry. It is forcing the insurance industry to pay for medical procedures with your insurance premiums, not advertising.

Third, it forces insurance companies to allow people with preexisting conditions onto health care plans.

This alleviates a lot of problems that our health care industry was facing. However, socialism is a government owned industry. Since the government isn’t owning anything, this definitely isn’t socialist.

So why is this not a point in the cards for Romney? Because Obamacare is demonstrably better than pre-Obamacare. And Romney’s only plan is to repeal Obamacare. He needs to have SOME plan to replace Obamacare - because going back to the way it was is untenable.

“So what are our options besides Obamacare? ” - GOP Supporter

Great question friend! There’s three things we can do (At least, that I can think of. Feel free to update me with your own).

Alleviate the problem by forcing people to pay for health care before they receive it. That way, costs will come down because everyone who gets health care will be insured. Hospitals will know that they can charge the actual costs of the procedures because they’ve already been paid. Everyone will be forced to buy insurance, because without it they’ll simply die. (This is assuming we could convince hospitals not to treat people for free anyways) This is the system of health care that places like Somolia, Uganda, Ethiopia, and other heavily impoverished nations with terrible quality of life have. If you have money, you live long, if you don’t, you die young. In my opinion, this is completely fucking unacceptable for the United States.

Socialized Medicine. *gasp*. This makes sure every single person pays into the system what they can, through taxes. And since every person is paying, every person can get health care. *THIS* is what we need, since every other country that is using it has a vastly better health care system. But that’s a different story. Read about the different types of socialized health care here.

Continue with the pre-Obamacare status quo. I’m not an economist and I don’t have any formal training in health care administration, so this is entirely conjecture: Prices will continue to rise which will force more people out of the insurance pool. This will cause health care prices to go up faster. Employer prices will continue to rise, either forcing an increase in the costs of goods, or forcing down salaries to compensate. It’s an all around fuck fest.

Quick Aside: I’ve been told that if we completely deregulate the health care industry and let the free market fairy sprinkle its magic all these problems will go away. Frankly this argument is full of shit. First, the problem of everyone being covered but not everyone paying still exists without another insurance mandate. Second - the free market decided that people with pre-existing conditions wouldn't be covered because it’s not profitable to cover them. That’s a whole group of people who don’t get health care - which in my opinion is equally untenable.

Of course, this is a simplistic view of the situation, and ignores a lot of important facts: Regular checkups and a relationship with the same physician is extremely beneficial for the health of the population, treating patients in a doctors office is cheaper than in the ER, access to vaccinations and health care earlier will result in healthier children, etc. Honestly I’m very lazy and want to go to bed, so I made this as simple as possible.

But it remains you *shouldn’t* vote for Romney while he advocates path 3 for our country. Obama really screwed the GOP hard by enacting Obamacare. By *compromising* and implementing the only possible solution that the right could come up with (a federal insurance mandate), he stole their only solution for health care. Once repealed, the only option the right has is to Re-implement Obamacare,

If you are a GOP supporter? Demand from your party a plan of action. Because without Obamacare, the health care industry is largely up shits creek. Moral arguments aside, it isn’t fiscally responsible to vote for Romney because of his lack of medical plan. As always I’m open to questions.

Why am I littering your dash with mind-numbing insurance crap?

Because the world of health insurance is complicated, and you can still lose everything if you have coverage and fail to navigate it correctly.

Even if your eyes glaze over instantly at the subject, I suggest you bookmark this as a future reference, because you either have your own insurance now, or you will someday soon, and there isn’t anybody who doesn’t need this knowledge. (Yes, I know there’s a double negative in that sentence. This is a financial post, not a grammar post.)

If you think this is valuable info, I ask you to please share it. You could help somebody save money/sanity.

My cred:

I write health plan docs for a living. I’m an Obamacare expert. I help clients with plan design, so I know the tricks. I implement federal mandates from HHS, IRS, DOL, and state agencies in order to keep my clients legally compliant. I know how to avoid penalties and coverage gaps. I know the tricks of plan design that are implemented to save employers money. I know which laws apply to which types of plans. I know how many ways participants can get severely burned if they don’t know how this works.

1. Your network is everything.

Never visit any type of practitioner without first checking if they are in your network. This is gospel. Many plans have separate INN and OON deductibles and out-of-pocket maximums that do not accumulate together. Some plans have an unlimited OON out-of-pocket limit, so you can still go completely bankrupt if you go OON.

Most plans have network provisions that will cover some OON providers at the INN level: emergency services until you’re stabilized (this is a federal mandate for non-grandfathered plans), No Choice of Provider provision if ancillary services are performed OON (e.g., if an INN physician sends your labs to an OON facility), and various out-of-area provisions. If you don’t know, call the customer service number and ask.

Physicians join & leave networks all the time. Even if your doc isn’t listed in the most recent Provider Directory, it never hurts to ask.

Many plans also have wrap networks that will negotiate with OON providers and facilities, so if all else fails, ask if your plan utilizes one of these to negotiate on your behalf.

2. Understand when your deductible accumulates & resets.

Your deductible is the amount of $ you pay for all services & prescriptions (except mandated preventive care on non-grandfathered plans) before your insurance pays a dime. This is in addition to the $ you pay for your premium. If you’re on an HDHP (high deductible health plan) or CDHP (consumer-driven health plan), your premiums will be very low, but your deductible will be very high. I’m on an HDHP, and my individual deductible is $2,600. Steep.

Deductibles usually reset every January 1, but some plans run off-year. Know your dates. If you’re on an HDHP, use the hell out of the HSA (health savings account) if available.

3. Preventive care is free!! Woohoo!!

The Affordable Care Act mandates certain preventive services be covered with no cost-share.

These lists are updated frequently, and new services are added every few months. My $500 Mirena IUD is now covered 100%, and the deductible is waived. The HPV vaccine is now covered for everybody between age 19-26. Depressing screening is covered. Tobacco cessation, immunizations, STI screening & counseling….all covered.

4. Preventive care isn’t free under every plan! Booo!!!

If your plan is grandfathered, they will likely opt to cover preventive services at the general benefit percent. The deductible will also apply. They are still allowed to exclude any preventive services they want.

Your plan document will (should) state whether your plan is grandfathered or not. If the doc is silent, call the carrier’s customer service line and ask.

5. Assume every EOB/bill you receive has at least 1 error, ESPECIALLY on hospital visits.

For the most part, claims processors have ZERO medical background. They’re paid just above minimum wage and are paid based on how many claims they process per hour. So you can guess how often errors happen.

I just had a preventive OBGYN claim come back as not covered, even though it should have been covered at 100%. If I didn’t know about the PPACA mandate, I would’ve just paid $219 out of my own pocket for an office visit that is supposed to be free.

You are paying enough/too much already for your premiums and deductibles. Make damn sure your claims are being processed and paid correctly. Raise hell if not, and get familiar with the appeals process.

6. Check your Medical Plan Exclusions before you go for any service.

Can’t stress this one enough.

7. Some plans offer surprisingly generous benefits such as 3-D mammography, genetic/genomic testing, acupuncture, and bariatric surgery.

Look at your Schedule of Benefits, but also check your Covered Charges for details on coverage and limitations.

There are federal mandates like the WHCRA, which requires all plans to cover the cost of breast reconstruction after mastectomy. Your plan document should have a section that lists federal notices.

The Mental Health Parity & Addiction Equity Act also requires plans to cover mental health & substance abuse services & facilities at the same level as the medical services & facilities. For example, a plan that covers a skilled nursing facility (medical) must also cover a residential treatment facility (MH). This is a bigger deal than it probably sounds like.

8. Check pre-certification requirements.

This is a cost containment strategy, and a lot of people aren’t even aware that covered charges are often denied/penalized if you don’t obtain pre-cert before the service. Again, check your plan document or call customer service. The most common services requiring pre-cert are: all hospitalizations (excluding routine labor/delivery), surgical procedures, transplants, clinical trials, outpatient rehab therapies, chemo & radiation, speciality drugs, home health care, durable medical equipment, prosthetics, and advanced imaging (MRI/MRA, CT scan, nuclear imaging, etc).

Any penalties you pay for failure to pre-cert won’t apply to your out-of-pocket maximum, so they really super suck. Some plans outright deny all claims for services that aren’t pre-certed.

9. You shouldn’t go broke.

Under PPACA, your in-network out-of-pocket maximum is limited. This means that you will never spend more than that amount in any year for covered services received from an in-network provider. The key here is the network, which I have to mention again since it is so critical.

Watch your EOBs carefully and monitor your accumulators (deductible and out-of-pocket limit). You can’t rely on the claims processors to get it right. I know it sucks and isn’t fair, but it’s the reality, and it’s your money on the line. There isn’t a claims processor or appeals lawyer in the world who will care more about your money than you do, so it really is up to you to be aware.

Godspeed, friends, and good health to you.

THIS NEEDS MORE NOTES

As much as this advice needs to be spread, it makes me so fucking furious that we live in a country where it needs to be spread.

And PSA #1 works adequately (I am not going to say well, because I think in/out of network is some of the worst of the bullshit of US health insurance) for most uncomplicated physical health needs.

Mental health? Not so much.

And if you get charged for failure to pre-cert, that’s the doc’s fault and you shouldn’t be responsible for the charges.

Also if you do get misbilled, don’t pay it - call to complain first, then ask if the doctor can submit anything to help

I once spent a year and half fighting an mri bill that they incorrectly labeled as frivolous until a doctor got involved

Also: keep calling. Get it in writing if you can. I just had a medically-necessary pre-cert-required drug not counted against my annual deductible (and our work shoved us all on high deductible plans which is SUPER GREAT for a family with 3 disabled people in it) because despite my calling multiple times and being assured it was taken care of, my pre-cert wasn’t done. Then I was told I could just pay for it out of pocket, and they would go back and count the drug against my deductible after the fact.

HA HA HA HA LIARS.

Also in my area the hospital is in-network but the ER doctors are out of network.

Workplace human error is a component of most businesses. Whilst some of these mistakes may be harmless, others could be costly both to your finances and to your reputation.

Because humans aren’t like machines, there’s no easy to fix to workplace human error. However there are things you can do to reduce it and make it less harmful.

Here are just a few tricks to help you reduce workplace human…

Employee benefits can make you stand out from other employers. If you want to attract and retain the right people, there are five employee benefits you should be offering.

Something that adds value to any employment position is employee benefits. When an employee signs up for a job with you, they expect to receive compensation in addition to their salary.

Suppose you have an unhinged neighbor who wants to burn down your house. You’d probably spend much of your time making sure that that doesn’t happen. Drafting plans for a megamansion you hope to build where your house once stood probably wouldn’t be a priority. But that seems to be the approach of some Democratic aspirants for the presidency, who spent big chunks of their recent debates arguing about details of costly “Medicare for All” plans that have no chance of becoming law. Our view.

KEEP INSURED: Homestead Fire Insurance Company issued this Map of New York City as a promotional piece in the 1860s or ‘70s under the slogan “Keep Insured.” The hand-colored lithograph wall map shows Manhattan from the Battery to the northern end of Central Park, along with a section of Brooklyn and Roosevelt Island. The map is decorated with engravings of the company’s Nassau Street headquarters and a small illustration of firefighters putting out a blaze. Tell us you saw it here and get a 20% discount! More here: https://georgeglazer.com/maps/newyorkmaps/homestead.html

I want to keep the person and entity they work for anonymous at the moment to avoid any legal/personal problems to them, but this story is horribly frustrating, specially if you’re dealing with chronic pain and how some doctors treat us.

The person we are talking about is REAL and got injured at work while lifting something heavy, which the person has done before, and here is what the “physician”( which the person in charge is a Physician Assistant (PA) and not an MD) where the patient is being treated at and people in that facility have done:

-The PA noticed the patient having SEVERE shoulder and chest pain, which she attributed to the patient having Pneumonia. The issue with this was that the patient was taken to the ER right after her injury by her company, her test weren’t consistent with pneumonia, and the PA disregard that and still left it in that paper work and did not provide with treatment or further blood test.

-The PA then said what the patient had was a shoulder injury that was acute, she did not provide more information and still left Pneumonia as a diagnosis. She did not want to provide with pain medication and sent patient to the ER.

-The PA sent a replacement doctor to work on the patient and the new doctor told her that her diagnosis of Pneumonia and acute injury in the shoulder was wrong, that the problem was a cervical injury, which once again she still left things as they were and ordered an MRI of the shoulder blade, and did not want to explore the possibility of a cervical injury.

-The patient went to her regular primary physician and asked for his opinion, he also agreed it was a cervical injury, which could happen after repetitive movement, he advice an MRI of the cervical area, which was not going to be approved and would be expensive.

-The patient got a shot, and was NOT informed of the purposed of it, the possible side effects, or what else to expect. The patient got a reaction to the shot, in which I got involved and went to talk on their behalf. I was upset at the fact that they were she COULD get a flare up due to the shot and they did not mention it, they sent the patient back to work. She retracted and said she did not ordered it and later gave her a window of a week of no work to recover from the flare up, this physician was nice compare to her usual one.

-The PA would get so mad at what happened and blamed the patient, then sent the patient to work and told her if the injury was not in the shoulder, like she wants it to be, she would not continue to see her.

-The PA told the patient not to return to her until MRI of her shoulder was done to get results.

-The PA noted that the patient asked for Tramadol, after being given some by another physician, and that the patient was rude and angry because they would not be given Tramadol, which was a lie. I was with the patient when the patient reported that Tramadol got her sick and not to be given anymore. So the PA lied..

-The receptionist laughed at patient.

-The PA canceled patient’s appointment without calling before hand.

-The PA mentioned how she was over-reacting about her pain and not to go see her face for nothing else.

-The PA called the person’s work manager to let them know that they could go back to work, without telling the patient, and telling the patient to not go to work until MRI results.

-Patient has MRI was was told they did the wrong one, luckily it was a cervical one that they did for mistake, the patient did show a cervical injury, but they twisted the story and said that the cervical injury was not related to the work injury and was not that much pain. A cervical injury could be caused by the movement she made at work, therefore what the doctor said was wrong, and patient went to a specialist to ask.

This is just the short version, for one I do not get how they label patients as liars, how they want them to “deal” with pain in useless physical therapies or tell patients to “forget” their pain.

I for one want to help this person and I am looking for all the options, but to me this is a legal matter now, but wanted to really help in letting them know that their pain matters, it isn’t fake, not just because you can’t see it from the outside.

“Protecting your privacy can be a difficult task in today’s world of information technology. With surveillance cameras on every corner and a recording device on every smartphone, there’s a good chance your image has been captured somewhere without you even knowing it. Safeguarding your mug in the future is set to become even more difficult with advancements in facial recognition technologies and wearable computers like Google Glass.

So what can you do to ensure your identity remains intact? In Western countries the answer would be simple: put on a pair of sunglasses. In Japan, however, sunglasses are a much less common sight, and many consider them to be worn only by those trying a little too hard to look cool, and in more extreme cases associate them with the yakuza lifestyle. Researchers at the National Institute of Informatics in Tokyo have addressed this issue by designing a non-threatening pair of white shades to protect both your identity and your public image, dubbing them the “Privacy Visor”…”

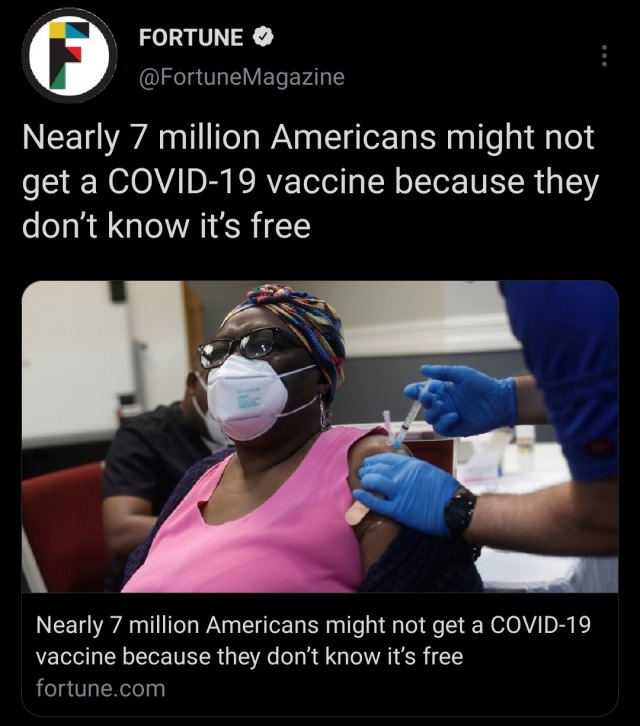

My sister, who I live with, thought she couldn’t get the vaccine because she doesn’t have insurance.

We’re not really used to “free”…. spread the word.

It depends where you go too. I tried to sign up at CVS and it said “free with insurance”

In the US they are not allowed to charge an individual for this vaccine. They are allowed to bill your insurance. Whether you have insurance or not, you will not pay anything.

THERE WILL BE A QUESTION ON THE REGISTRATION ABOUT INSURANCE YOU DO NOT NEED TO FILL IT OUT.

When I registered there was a page for insurance information. We were instructed just to put “no insurance” and keep going.

Motor insurance policies is necessary to generate a motor vehicle lawfully. It is various from motor trade insurance policy. What does it consist of, how does it function, what are the diverse sorts of vehicle insurance?

Motor insurance: a obligatory stage

Since auto has been a lawful obligation for any driver wishing to journey, and more typically in a distinct geographical region (DOM-TOM, Europe, and so forth.). The primary operate of motor trade insurance policies is to give compensation for injury that may be caused to a third celebration by a driver and / or 1 of his passengers. It handles the fees incurred for accidents triggered to an person (clinic care costs, and so on.) and in case of materials harm (on other vehicles, but also on true estate, and many others.). Driving an uninsured vehicle is an offense punishable by regulation. It could result in a fine, suspension of license or even impoundment of the automobile involved by the offense.

The basic principle

Auto insurance coverage is a basic time period. There are numerous circumstances beneath which these insurances are covered. It aims at a number of possible ensures:

the most crucial, the RC Auto (lawfully known as Civil Liability for Motor Automobiles), which covers the legal responsibility of drivers of a vehicle. This insurance policies is necessary for all motor vehicle owners as soon as the automobile is set into circulation on the “community freeway”. When you are responsible for an incident, this insurance policies handles content and bodily harm to the victims but does not cover your own individual injuries or residence hurt to your car. For this purpose, AutoCar is frequently supplemented by other covers. omnium and mini-omnium covering the materials injury caused to the insured automobile

the lawful defense that handles lawful charges and brings the insured help and guidance in lawful matters

driver’s insurance policies covering the bodily damage endured by the driver

the help , which enables to supply assistance to the insured in circumstance of failure of the vehicle (repair, towing).

Other insurance coverage can also intervene in the context of a car accident. This can be the scenario:

workers’ payment insurance policies covering the employee for accidents taking place during operate and on the way to function

Mutuals, who shell out for certain healthcare costs, especially when you are accountable for an incident and you are hurt as a driver

Getting auto insurance

There are several insurers these days, a single of whose principal missions is to provide drivers car insurance policy. The auto insurance policies plan (ensures offered, alternatives, rates, and so on.) differs from a single driver to yet another. The large greater part of insurers consider into account the expertise of the driver ( younger driver or seasoned driver), but also the quantity of kilometers traveled in the 12 months, the kind of motor vehicle insured (town car, luxurious sedan, and many others.). , the driver’s liability (amount of accidents encountered in his driving existence), etc. It is consequently quite critical when deciding on an vehicle insurance policy to evaluate provides. In current many years, the trend in the subject of motor trade insurance coverage is also transferring in the direction of a maximum of “tailor-created” to reduce the rates for excellent drivers and boost the charge amid unsuspecting motorists on the highway. It has turn into little bit much more personalized.

Assures of motor insurance

In addition to the obligatory legal responsibility insurance policy (and distinct from the civil liability of the private existence), the automobile insurance policy can propose numerous guarantees more or considerably less helpful according to your circumstance. There are traditional safeguards such as “broken glass” or safety in opposition to theft and fire, but also other a lot more specialized ensures this kind of as the “normal disaster” guarantee. As with any variety of insurance policies agreement, it is advised to review meticulously the clauses and the assumption of responsibility of these ensures ahead of subscribing to them.

The guide is now live. Thank you to everyone who provided feedback and offered improvements on the original draft.

If you like what I do and want to support me, you have a bunch of cool options:

Stop scrolling, click on the link and actually read what I’ve written on my site. This helps improve my Google rankings and grow my audience. Tumblr does nothing but steal my content and traffic.

Reblog this article (after you’ve read it) and help spread the word.

Upcoming Post: How to Buy a Wheelchair Without Insurance

I’m planning on writing a guide to help people navigate buying a wheelchair without insurance (primarily aimed at US readers).

What I need from you: tell me about the struggles and barriers you encountered (other than finances) when trying to purchase a chair for yourself when insurance wouldn’t cover it.

Feel free to share and reblog as needed, but please don’t respond unless you’ve gone through (or tried to go through) the process of buying a chair without support from insurance. Tumblr conversations are hard enough to follow as it is.

If you wanna submit an anonymous ask replying to this (or use the Ask form on my main site), feel free. Just let me know that this is the post you are referencing.

The guide is currently live on my Patreon. As always, I’m looking for feedback on what’s missing or what could be improved. Once folks have had a chance to look at it and provide feedback, I’ll put it up on my main site.

Upcoming Post: How to Buy a Wheelchair Without Insurance

I’m planning on writing a guide to help people navigate buying a wheelchair without insurance (primarily aimed at US readers).

What I need from you: tell me about the struggles and barriers you encountered (other than finances) when trying to purchase a chair for yourself when insurance wouldn’t cover it.

Feel free to share and reblog as needed, but please don’t respond unless you’ve gone through (or tried to go through) the process of buying a chair without support from insurance. Tumblr conversations are hard enough to follow as it is.

If you wanna submit an anonymous ask replying to this (or use the Ask form on my main site), feel free. Just let me know that this is the post you are referencing.

Interview by Meg Wachter Illustration by Amanda Stosz

A month ago on bus ride from New York City to Washington DC I befriended the woman across the aisle from me as we discovered we were both on our way to attend the first ever (in 2016!) White House sponsored: The United State of Women Summit. We were to attend along with 5,000 other women from across the country to discuss economic empowerment, leadership and civic engagement, educational opportunities, violence against women, entrepreneurship and innovation, and health and wellness. It turned out that Jeanne Pinder, a former veteran reporter at The New York Times, falls in the two later categories. She went on from a lifelong career in journalism to creating ClearHealthCosts–a start-up that brings “transparency to the health-care marketplace by telling people prices for medical procedures and items. By revealing prices, we are empowering consumers to make informed decisions about the costs of their medical care and coverage.”

“There’s no easy way to know prices, or to make smart decisions with your money and your health. We’re working to change that.”

Hey Jeanne! Can you tell us a bit about yourself? What’s your background?

I’m a journalist, a believe in full-on transparency. Like all journos, eager to afflict the comfortable, and comfort the afflicted. I’m a native Iowan, living just outside of New York City. Single mom of amazing twin girls, now 22 and just graduated from college.

How long were you a reporter at the New York Times? What led you to a life in journalism? What was/is your favorite thing to cover?

I was born into a newspaper family: My first job, at 13, was as a cub reporter at The Grinnell (Iowa) Herald-Register, a twice-weekly community paper. My dad (who married the boss’s daughter!) was the editor. I grew up there, and worked my way through Grinnell College at the paper.

After earning a BA in Russian, I tried to get out of journalism by going to graduate school in Slavic linguistics, but it didn’t stick and I went back to journalism.

After stints at The Associated PressandThe Des Moines Register, and almost two years living in what was then the Soviet Union, I was hired as an editor at The New York Times.

The Times is a great place to work. I was there for almost 25 years – first, for almost 10 years, as an editor on the Foreign Desk, specializing in Soviet and East European affairs, during the fall of Communism. It was an amazing run of news: The Berlin Wall went down, freedom flowered and then was crushed in Tiananmen Square. The wars in the Middle East, the end of apartheid in South Africa – I got to work with the smartest people in the world on foreign affairs at a time of epochal change.

After that, I was a reporter covering commercial real estate, the deputy founding editor of the Circuits Technology section, the “work-life manager” implementing a policy for flexible and nontraditional work schedules, an editor on the Metro section (during September 11 and its aftermath) and an editor on the lifestyle sections.

I volunteered for a buyout in 2009, and starting in late 2010 I won a series of grants and some angel investment to build ClearHealthCosts, a journalism startup bringing transparency to the health care marketplace by telling people what stuff costs.

I love big, complicated topics. The (then) Soviet Union, technology, nontraditional work arrangements and the crazy opaque health care marketplace.

Why is it important to bring transparency to the American healthcare industry and what was your journey to creating ClearHealthCosts? Was there anything in your life or anything in particular that inspired you to want to start CHC?

People should know what stuff costs. All prices should be clearly available in advance: the price charged, and how much you will pay, and how much others are paying.

That’s what we do at ClearHealthCosts: we find out and post health prices publicly. We use shoe-leather journalism and data diving to find stuff out about pricing and tell people. We also crowdsource health prices with big public media partners like KQED public radio in San Francisco and WLRN public radio in Miami. (Here’s a roundup of our partnerships).

A simple MRI can cost from $300 to $6,221 in the same metro area, depending on provider. But it’s hard to find that information.

Those birth-control pills could cost from $9 to $63. But how can you know?

The way it works now:

You: “I need an MRI. Here’s the prescription.” Office person: “Please give me your credit card.” You: “How much will this cost?” Office person: “We don’t know.” You: “Then why would I give you my credit card?”

So, our solution: We’re a mashup of Waze and Kayak for health care prices.

Where you’re able to make a choice – in common, “shoppable” procedures – we give you clear, actionable information, displayed in context.

You might need to know how much an abortion costs, or the price of a colonoscopy.

You might want to know that you can sometimes save money by paying cash – instead of using your insurance card. You might also want to know that there are a number of price transparency tools out there on the interwebs that are not very transparent.

There’s no easy way to know prices, or to make smart decisions with your money and your health. We’re working to change that.

You should be able to easily find out in advance.

It’s a national embarrassment: Our health care system takes advantage of people who are ill, or who don’t have gold-plated insurance, or who don’t have the time to fight through the murk and the bureaucracy and the active attempts to keep you in the dark about prices.

I got interested in this as a journalist because it’s a problem hiding in plain sight: No one can understand their health care bills and insurance company communications.

If it’s this hard to understand, you can bet someone’s making money off the information asymmetry.

As a 33-year-old woman with very bare bones health insurance, I have an extremely high deductible ($6k+) and therefore pay my monthly premium (around $260/mo) in addition to out-of-pocket for any doctor’s visits or procedures. Sometimes I wonder why I have health insurance at all. Why is our system so broken and when did that start?

I feel your pain!

Once upon a time, our insurance system made more sense. It was born of the knowledge that high medical bills can beggar a person, and the need to protect against that.

Our insurance system expanded after World War II, as a result of concern for workers’ welfare and the need to fill jobs, and the system became largely employer-driven for many of us.

This worked pretty well for a while, but then all the nonprofit insurers and other nonprofit market players began to turn into for-profits. This is in some sense a reflection of who we are as a nation – we love us our free enterprise! – but it doesn’t work that well in health care.

If a company is a sleepy, nonprofit hospital or mutual insurance company, it’s more likely to be worried about the welfare of its patients and its insured people.

If it’s a for-profit hospital, insurer, or drug company, answering to shareholders on Wall Street, it’s worried about the stock price. So, obv: if less money is spent on patients, more goes to boosting stock prices, to advertising and executive compensation, to dividends and other things that don’t directly affect the mission of patient care – promoting wellness and treating ill people. Here’s a particularly egregious example about Epipens, though the examples are many.

To be clear, I’m not an opponent of for-profit, free enterprise systems. I used to live in the Soviet Union, and that was an unspeakable mess.

What I think about for-profit, free enterprise health care is that all the prices need to be public, all the time, so I can know what my choices are.

Also: The health care system – like many other systems – is largely built and operated by men, and used primarily by women.

Women own reproductive health, pediatricians’ appointments and elder care. Women nag their spouses, whether those spouses are husbands, wives, or none of the above, to get their health issues taken care of. Men? When we talk about this topic, they often want us to know “no one cares what things cost in health care” or “I haven’t been to a doctor in 12 years” or “doesn’t it all cost $20 or whatever your co-pay is?”

It’s a huge disconnect. As in so many other things, the gender lens and the bias it creates serve to disadvantage women. (I wrote a bunch more about that here.)

What country has the best model of national health care?

Good question: People say that Singapore and Australia have a good blend of private and public, but I have no personal experience of either.

Some of the European social democracies (Denmark, the Netherlands, Sweden) also seem to have a happy solution.

Our system? It’s an international laughingstock: We spend more money and do worse on major measurements of success than any other nation – check out this study and charts. Gah.

What do you hope to achieve with CHC?

People should know what stuff costs.

All prices should be public, all the time: The charged price, your responsibility either as an insured person or a cash patient, what the insurer pays, what the government would pay for the same service.

Our current system is built on half-truths and secrecy. That has to stop.

What women inspire you? Who do you currently admire?

Ah! So many! Here are a few.

Michelle Obama Hilary Clinton Ruth Bader Ginsburg Sonia Sotomayor Patti Smith Pussy Riot Shonda Rhimes Jen Pahlka at Code for America Cindy Gallop Rachel Sklar and Glynnis MacNicol and the #badass Ladies of The Li.st. Aminatou Sow and Erie Meyer and the #badass women of the TechLady Mafia. Galina Timchenko at meduza.io Abbi Jacobson and Ilana Glazer at Broad City Malala Yousafzai Helen Mirren Nancy Lublin at Crisis Text Line

lottery tickets have negative expected value, but so does insurance, right?

The different is the risk associated. Insurance reduces your risk (smooths out the variance in your cash flow), so it has a value.

Same reason futures markets exist.

I don’t understand this. When you say it has a value, do you mean in the sense of raising the expected value of your future wealth? Or just that it’s good for something?

If money has decreasing marginal utility, the same sum of money is worth more to you when you have less money (because, say, you have a sudden unexpected expense).

Insurance increases your expected wealth conditional on certain events that (otherwise) cause a significant drop in wealth. Hence, it has a positive payout in expected utility, even though it has a negative payout in expected money, because it pays out specifically at the times when money has greater than average utility.

Putting money into a savings account than stocks is no different than insurance. Yet in real life it probably increase your expected wealth over time because equities probably goes down in value when you are least likely need to withdraw from it.

I’m not sure I actually believe that equities go down in value when you’re least likely to need them. Hence, lots of financial advice that you should keep an emergency fund with several months worth of expenses in liquid assets. Unless you mean that they’re only likely to go down in the short run and you’re more likely to need them in the long run, which is probably true at least for young people (and, again, note the general trends in financial advice, where suggested assets weights differ for people in different life stages).

But it’s certainly the case that the short term wealth shocks that people generally insure against can be MUCH greater in magnitude than the sort of wealth shocks you’re likely to see in (properly diversified) equity savings.

In any case, I don’t claim that you should make every “insurance-like” deal. Obviously, it’s possible for a sufficiently large difference in expect wealth to make them net negative in expected utility. Hence, equities for young people.

lottery tickets have negative expected value, but so does insurance, right?

The different is the risk associated. Insurance reduces your risk (smooths out the variance in your cash flow), so it has a value.

Same reason futures markets exist.

I don’t understand this. When you say it has a value, do you mean in the sense of raising the expected value of your future wealth? Or just that it’s good for something?

If money has decreasing marginal utility, the same sum of money is worth more to you when you have less money (because, say, you have a sudden unexpected expense).

Insurance increases your expected wealth conditional on certain events that (otherwise) cause a significant drop in wealth. Hence, it has a positive payout in expected utility, even though it has a negative payout in expected money, because it pays out specifically at the times when money has greater than average utility.

lol I am in such a stressed-out blind rage today from insurance bullshit that I wrote up a glossary of health insurance terms (things like deductibles, premiums, and copays) because all the free guides online are unnecessarily complicated and the only way you can squeeze a dime out of these bullshit companies is to understand their overly-complicated policies. give em hell

This is a GREAT guide folks - it’s simple, straightforward, and deals well with the overly complicated alphabet soup of medical insurance. Knowing this stuff can prove REALLY helpful, and the examples used are a great resource.

Will someone explain to me why vision and dental care are not considered part of medical care in the USA?

It can’t be because they’re not medically necessary, at least not with any consistency. There’s a lot of stuff that does fall under medical, and is sometimes covered by medical insurance, but is either not medically necessary or is less so than maintaining vision and dental health.

This just doesn’t make any sense. I could go to a dermatologist about mild skin imperfections that are not a disease and not a problem other than being slightly ugly, and get those treated under medical insurance. But medical won’t cover extracting a broken wisdom tooth before it gets infected, or even preserving ability to chew food. It won’t cover correcting vision. So medical care doesn’t cover tooth problems that can cause pain, infection, and even (if extreme enough) life-threatening disease, and doesn’t cover simple, cheap diagnostics and devices to correct the most common mild to moderate visual disabilities. Teeth and eyes are body parts!

I don’t get it.

When I was doing volunteer archival work, I came across an oral history transcript where the speaker talked about trying to go around convincing dentists to sign up for this newfangled “dental insurance” thing. I believe this was happening in the 1960s. It seems that dentists joined the Health Insurance bandwagon many decades after doctors and hospitals got it going.

When I asked my dad about this, he said that for a long while, most people did not consider dentists to be Real Doctors, even after their techniques gained a measure of sophistication and safety. So it may be that long-standing prejudice delayed dentists from being included in Health Insurance for long enough that by the time it was possible, it was too late because dentists had all joined their own thing.

Not sure about the vision care. Possibly the same process in later decades. The point is, health insurance in the U.S. has as much to do with Path Dependence and getting stuck in 20th-century nationwide mistakes as it has to do with rational incentives.

Ooh… yeah, that could do it. Bureaucracy and path dependence. Lord knows the health insurance situation is weird and complicated. Thanks for the info!

It’s kind of depressing because this seems like it would be fairly simple to fix and I guess it isn’t. There are a lot of people without health insurance, but more have to go without vision/dental coverage than go without basic medical coverage. So one way to at least reduce the problem would be to fold vision correction and not-primarily-cosmetic dentistry into medical. It wouldn’t raise costs much and would save a lot of people’s teeth and vision. Perhaps the dental insurance and vision insurance companies would howl and scream too much and it would keep us all from sleeping. :(

Health insurance must be owned if you have a serious medical emergency. You never know when a disaster will attack in the form of disease, accident or injury. If you are not ready with a good health insurance plan, you can lose everything. If you have a good health plan in its place, you can calm down so that your expenses will be taken care of. You have several choices in terms of buying health insurance. You can use an individual package, or if your employer offers group insurance, you can save money by choosing the package.

When it’s time for you to update your policy, check your current plan to verify that you still need all the services you pay, and that you have enough scope. What works for you in the past may be inadequate now, especially if your health has changed or you need to add someone to your scope. You can also make changes to the vision, teeth and other insurance options.

Vision of Makess Insurance feels for you and your family, especially if there are people who have problems with vision, or eye problems that are run in your family. Insurance vision includes some of your eye tests and will also pay at least a portion of your contact lenses or purchase glasses. You are not required to bring vision insurance, so if no one in your family suffers from eye disorders, you can save money by releasing it.

Every year, check to see which recipes are covered. Every year, when you re -register in your insurance package, your insurance company has the right to change the planning of the plan. Read all documents when you re -register and ask your insurance agent to clarify whatever you are confused. In particular, pay attention to the prescription drug covered by your plan and pay attention to changes that may occur from year to year. If the medicine you rely on every day is no longer covered, you might need to find a new insurance operator.

Beware of your tax credit for health insurance bills. Your health insurance premium can be deducted from taxes. Every money you spend to cover up your reduction, your recipe, or any visit that is not covered by your insurance can also be deducted from your taxable income. Because state and federal tax regulations vary for this reduction, you want to examine your country’s guidelines first.

When you apply for insurance, the company will call you. Make sure you don’t donate any information they don’t ask specifically. Answer only their direct questions. When you voluntarily too much information, the results can be an increase in your premium, or the worst, complete rejection of coverage.

By comparing group and individual plans, you can say that while one might be cheaper, the other can offer more choices. In both cases, the important thing to remember is that you must have at least several forms of health insurance. Being without health insurance in this day and age leaves the door to open for problems. Life can come to you quickly, and a sudden disease or accident can find you draining your life savings in a short time. Don’t let that happen to you. Look at the proper health insurance option immediately.

Let’s get real on health care Suppose you have an unhinged ne")